A few years after this post appeared, a paper appeared on the same topic, analyzing 4 different Bitcoin bubbles.

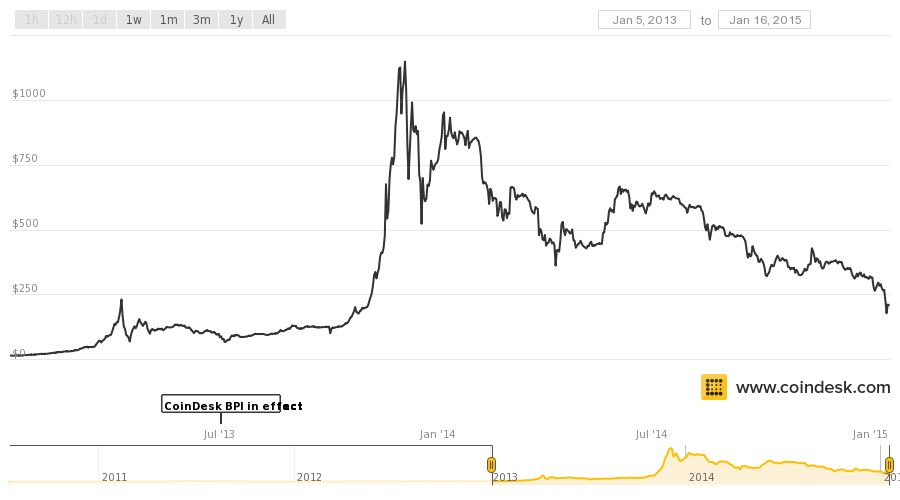

On Jan 14, 2015 Bitcoin dropped below $200 (USD)

Moreover, several Bitcoin exchanges have shut down due to hacks and/or criminal activity, and key BitCoin players are on trial. This begs the question:

Why is BitCoin Crashing ?

Markets crash all the time. Stock markets. Currency Markets. Even the Dutch Tulip market of 1637 crashed–although even this is still hotly debated.

Fraud? Speculation? Mania? Lack of Regulation? What gives?

Market Crashes: the EconPhysics Perspective

In 1996, researchers at the University of Chicago[1] and elsewhere [2] independently proposed that market crashes resemble physical crashes such as earthquakes, ruptures, and avalanches. Such phenomena arise from long range, collective fluctuations — i.e. herding behavior — that overtakes a system as it approaches a critical point…and/or in the aftershocks.

![Discrete Scale Invariance in the SP500 Crash of 1987 [1]](https://charlesmartin14.files.wordpress.com/2015/01/sp500_rg.png)

Most notably, the strongest proponent, Didier Sornette, accurately estimated the long bear run of the Japanese markets–what he terms a Financial Anti-Bubble:

He has written numerous papers, a book, and even a TED Talk.

We also introduced these ideas in a previous post: Noisy Time Series II: Earth Quakes, Black Holes, and Machine Learning

Power Laws and Symmetry Breaking

It is well known that financial markets display non-Gaussian, long tail, power law-like behavior. After a crash model, the price series itself

where

We can fit the recent Bitcoin EOD (End of Day) prices to a power law, starting at it’s peak on Nov 11, 2013:

We obtain a modestly good least squares fit, with

RG theory suggests that near a crash, the power law may become complex (i.e a form of ‘symmetry breaking’). We will now sketch how this comes about, using the nobel prize winning Renormalization Group theory.

Complex Power Laws and the Renormalization Group

When examining a price series

Here, we will find that as

where

We say

We also know that near a critical point, physical systems exhibit scale invariant (i.e. fractal) behavior. The noise, or fluctuations, we observe on small time scales

We call

The fundamental RG equation (eqn) is:

We assume

The magic of the RG theory is that it allows us to describe the behavior near a critical point knowing only the flow map

![f^{n}(x)=\sum_{i=1}^{n}\dfrac{1}{\mu^{i}}g(\phi^{[i]}(x))](https://s0.wp.com/latex.php?latex=f%5E%7Bn%7D%28x%29%3D%5Csum_%7Bi%3D1%7D%5E%7Bn%7D%5Cdfrac%7B1%7D%7B%5Cmu%5E%7Bi%7D%7Dg%28%5Cphi%5E%7B%5Bi%5D%7D%28x%29%29&bg=ffffff&fg=%23000000&s=0&c=20201002)

We present a leading order approximation to

RG Theory and Discrete Scale Invariance

We start by first assuming power law behavior (at lowest order):

We seek the simplest RG solution. Let us assume the RG flow map is linear in

where

We ignore the regular solution

For our simple power law, we have

This is easy to satisfy if

or

We seek the most general solution, applicable to discrete physical systems, such as earthquakes, ruptures in materials–and financial market crashes. That is, we expect

![\lambda\in[\lambda_{1},\lambda_{2},\cdots]](https://s0.wp.com/latex.php?latex=%5Clambda%5Cin%5B%5Clambda_%7B1%7D%2C%5Clambda_%7B2%7D%2C%5Ccdots%5D&bg=ffffff&fg=%23000000&s=0&c=20201002)

We call this Discrete Scale Invariance (DSI)

The most general solution of DSI is

where

![P_{n}(x)=\sum_{i=1}^{n}c_{n}\exp\left[2n\pi i\left(\dfrac{\log x}{\log\lambda}\right)\right].](https://s0.wp.com/latex.php?latex=P_%7Bn%7D%28x%29%3D%5Csum_%7Bi%3D1%7D%5E%7Bn%7Dc_%7Bn%7D%5Cexp%5Cleft%5B2n%5Cpi+i%5Cleft%28%5Cdfrac%7B%5Clog+x%7D%7B%5Clog%5Clambda%7D%5Cright%29%5Cright%5D.&bg=ffffff&fg=%23000000&s=0&c=20201002)

This is a classic Weierstrass function–a pathological function that, in the infinite limit, is continuous everywhere and yet differentiable nowhere. It is used to model fractals, natural systems that are scale invariant, and highly discontinous but structured time series.

In a crash scenario, we expect that the true power series for

![exp\left[2n\pi i\left(\dfrac{\log x}{\log\lambda}\right)\right]](https://s0.wp.com/latex.php?latex=exp%5Cleft%5B2n%5Cpi+i%5Cleft%28%5Cdfrac%7B%5Clog+x%7D%7B%5Clog%5Clambda%7D%5Cright%29%5Cright%5D&bg=ffffff&fg=%23000000&s=0&c=20201002)

Note that it takes the form

so

We now see that we have a complex critical exponent

or

We consider the real part of the complex power law

![Re[x^{\alpha+i\beta}]=x^{\alpha}cos(\beta\log x)](https://s0.wp.com/latex.php?latex=Re%5Bx%5E%7B%5Calpha%2Bi%5Cbeta%7D%5D%3Dx%5E%7B%5Calpha%7Dcos%28%5Cbeta%5Clog+x%29&bg=ffffff&fg=%23000000&s=0&c=20201002)

which gives the following log periodic formula for the price series

Instead of fluctuating randomly around the underlying power law drift, the price series exhibits log-periodic oscillations–the DSI signature of a crash.

This model appears to work for 1-2 oscillations before (or after) the crash. To model the longer time anti-bubble behavior, Sornette has developed an extended formula, based on the third-order Landau expansion (as opposed to, say, additional terms in the power series defined above). We leave these details and further analysis for later.

DSI Fit of the Bitcoin Crash

We now fit the latest Bitcoin behavior, assuming the crash / Bear market started on Nov 29, 2013 :

We readily find a DSI fit, with

It is actually quite difficult to get a very tight fit, and usually advanced methods are needed. This is a simple, crude fit done to illustrate the basic ideas.

We see that Bitcoin, like other financial markets, displays log periodic behavior, characteristic of a self-organized crash.

These kinds of crashes are not caused by external events or bad players–they are endemic to all markets and result from the cooperative actions of all participants.

We can try to detect them, perhaps even profit off them, but it is unclear how to avoid these Self-organized Critical points that wreck havoc on our finances.

Conclusion: How Nature Works

Bitcoin is an attempt to create a new kind of currency–a CryptoCurrency–that is free from both institutional control and individual corruption. It is hoped that we can avoid the kind of devastating inflation, devaluation, and crashes that occur all too frequently in our current worldwide banking systems. The promise is that Bitcoin, backed by the Blockchain, can remove our dependence on a single, faulty institution and replace it with a decentralized, distributed form of trust. But

“Real life operates at a critical point between order and chaos”

Our analysis here shows that even the Bitcoin economy still appears to behave like a traditional market–prone to kinds of crashes that frequently arise in all natural self organized systems.

This Self-Organized Criticality is perhaps just how nature works [6,7].

And while Bitcoin is certainly interesting and exciting, perhaps it too is subject to the natural laws of physics.

References

[1] 1995 James A. Feigenbaum and Peter G.O. Freund, Discrete Scaling in Stock Markets Before Crashes

[2] TED Talk: How We Can Predict the Next Financial Crises

[3] What will upend the economy next? Economist didier sornette explains

[4] D. Sornette, Critical market crashes

[5] 1999 Predicting Financial Crises using Discrete Scale Invariance

[6] 1999 A. Johansen and D. Sornette, Financial “Anti-Bubbles”: Log-Periodicity in Gold and Nikkei collapses

[7] Anders Johansen and Didier Sornette, Evaluation of the quantitative prediction of a trend reversal on the Japanese stock market in 1999 , 2000

[8] 2003 Wei-Xing Zhou and Didier Sornette Renormalization group analysis of the 2000–2002 anti-bubble in the US S&P500 index: explanation of the hierarchy of five crashes and prediction

[9] 20122 Didier Sornette, Ryan Woodard, Wanfeng Yan, and Wei-Xing Zhou Clarifications to Questions and Criticisms on the Johansen-Ledoit-Sornette Bubble Model

[10] http://guava.physics.uiuc.edu/~nigel/courses/563/essay/lin.ps.gz

[11] Per Bak, “How Nature Works: The Science of Self-Organized Criticality”, 1996

also related on the Sornette works

LikeLike

Came across your blog by accident; nice work! I had done a similar analysis of the first bitcoin crash, though my interests changed over time and I hadn’t followed later crashes. I should probably be doing this in real time…

LikeLiked by 1 person